Sanjeel Kothari – I am currently doing FinBridge program from Finnacle Investment Academy, Surat. I have cleared CFA Institute’s Investment Foundation exam. My ambition is to become Equity Research Analyst.

Understanding Total Addressable Market’s Research Paper

TAM is defined as the revenue a company could realized while having 100 per cent market share while creating shareholder value. The ability to calibrate the total addressable market (TAM) is a major part of anticipating value creation.

This report provides a framework for estimating TAM through the process of triangulation. Three methods are used – first is based on population, product and conversion. Next diffusion model is analyzed in which addresses absolute size of market and also rate of adoption. Finally, base rate check is done for reality check.

Categorizing New Products

To assess market size categorization of product is a logical starting point. This allows us to appraise a company’s strategy to promote the product. Companies can influence their TAM through pricing strategy and product enhancement. Pricing strategy is when companies sell products at discount in order to gain market share. Product enhancement can reflect improvement in the product itself.

Current technologies that have applications for new customers and new technologies used by current customers are the categories where a TAM analysis is most relevant. TAM is tricky to analyze when both technology and customers are new.

Some specific ways to estimate TAM –

Market Size – Population, Product and Conversion

First approach is to estimate absolute market size, in which number of potential customers is multiplied with expected revenue per customer. There are three parts for this analysis – first is population in which we estimate the population which can use our product, second is product in which we estimate population which is likely to use our product and the last is conversion where we analyze what can be the potential revenue. Factors that shape up demand and supply can be considered for doing more in – depth analysis of absolute market size.

Factors to consider in assessing demand are financial resources, physical limitations, elasticity of demand, cyclicality, substitution and substitution threats.

Factors to consider in assessing supply are ability to supply, unit growth and pricing, regulatory constraints, incentives, scale, niches.

TAM and the Bass Model

The Bass model allows for a prediction of the purchasers in a period, say for each year, as well as a total number of purchasers. Bass model relies on three parameters –

- The coefficient of innovation (p) – This captures mass-market influence

- The coefficient of imitation (q) – This reflects interpersonal influence.

- An estimate of the number of eventual adopters (m) – A parameter that determines the size of the market.

The equation for the Bass model is – N(t) – N(t−1) = [p + qN(t−1)/m] x

This formula simply says that new adopter’s equal the adoption rate multiply the number of potential new adopters.

N(t) – N(t−1) shows the number of adopters during a period i.e. simply the difference between the users now, N(t), and the users in the prior period, N(t−1). First term on the right side of the equation spells out the rate of adoption. The second term on the right side is the number of users who have not yet adopted the product.

Investor application of the Bass model –

The first is to estimate product potential based on the parameters from historical diffusions. Second way to use the model is to start with a company’s stock price and backwards.

Bass model also allows solving for the size of peak sales. For calculating the size of peak sales this equation can be used –

Size of peak sales = m[(p+q)2 / 4q].

There are typically three stages in industry evolution. During the first stage, the number of competitors grows. In second stage there are large shakeouts as the result of higher number of firms exiting. In third stage, number of competitors and market shares stabilizes. In stage two company’s sales can grow faster as the numbers of competitors are reducing.

Limitations for Bass model –

This model can be helpful in judging TAM. But there are some limitations that don’t allow it to capture certain considerations.

First limitation is of replacement cycle. Bass model is used primarily for forecasting adoption of a product. But very less attention is given to replacement cycle. Replacement cycle talks about replacement of a product once the purchase is done.

Second limitation is of economies of scale. Economies of scale is when company’s fixed cost gets spread over higher sales i.e. when company do more sales then the fixed cost spreads over a larger base. This limits the level of TAM because companies fail to create value after a certain size. There is a separate issue with similar implications. This is when companies overshoot their markets. Two symptoms of overshot market are customers use only a fraction of the functionally the product offers and they are not paying for new features.

Third limitation is of network effect. Network effect is there when value of one product increases when more people start using it. Example – telephone. If only one person is using then it has very little value. But as more number of people starts using it the value increases. In businesses where strong network effect is there, market shares of companies are higher. Companies spend heavily in the hope that their product will become the product of choice but in sectors with strong network effects, most companies fail to go from early adopters to mainstream users.

Base rates as a reality check –

Third method in the triangulation process to estimate TAM is careful consideration of base rates. The main idea is to refer to what happened to other companies when they were in the same stage. This can be useful because, say for example, a company’s management is saying that they can grow at 10% CAGR in the coming 5 years. But in base rate method we check that what happened to other companies when they were in the same stage. This can be a reality check. Base rates provide a check on the output of the first two approaches to estimating TAM.

TAM and Ecosystems

Generally business can be in three categories – Physical, Service and Knowledge. Main objective is to understand the characteristics of these categories and to consider how companies can expand across them.

Physical – Main source of cash flow for these businesses is tangible assets like manufacturing facilities, stores and inventory etc. Sales growth is tied to asset growth.

Service – Main source of competitive advantage is people for service businesses.

Knowledge – These businesses also rely on people as their main source of competitive advantage.

These categories differ in economic characteristics. Some considerations are as –

Source of advantage – Physical companies depend on tangible assets while service and Knowledge business depend on people.

Investment trigger – Physical and service business can grow by adding capacity either in the form of CAPEX or new employees. Knowledge businesses generally invest to deal with obsolescence.

Products and Protecting Capital – Rival goods are those where consumption of one’s product will decrease the consumption of others. Non-rival goods are generally difficult to protect because they are relatively easy and cheap to replicate. Creator of a non-rival good often has difficulty capturing the value. One strategy companies use to increase TAM is to extend business in new business categories. This extension can have challenges such as trade-offs between open and closed systems, functionality in the product or in the cloud, determining which party owns the data, and whether or not to monetize data by selling to outside parties.

Understanding Value Migration’s Research Paper

This research paper discusses about value migration in 4 industries.

What is value migration?

Value migration is flow of economic value from old business model to new business model which are better able to satisfy customers. For example – Shifting of people from black and white television to colour television was value migration. For colour television industry it was value inflow but for black and white television industry it was value outflow.

Value migration happens in three stages –

Value Inflow – Companies or Industry is able to capture value from other industries or companies due to superior value.

Stability – Competitive equilibrium is established.

Value Outflow – Value move towards new industry or industry which are better able to cater needs of customers.

The four sectors covered in this paper are BFSI, Information technology, Oil and Gas, Consumer (Jewelry)

BFSI –

Shift is happening from public sector banks to private sector banks which are customer friendly. Corporate banking sector is facing challenges and public sector banks will face challenges on capitalization and growth. While private sector banks can emerge stronger because they have used digital capabilities and also expanded their branch network. They also have a strong traction in CASA mix.

Private sector banks have invested heavily in technology and have come up with various innovative products. Their CASA grew at fast pace. Also private sector banks have good digital architecture. They have higher share in digital transactions. Private sector banks have taken balanced approach. Through strategic partnership costs are under control and also profitability has been maintained.

For public sector banks, government announced recapitalization plan but most of the money will be used in provisioning requirement. FY 19 was in full compliance with Basel –III regulations; there was pressure on public sector banks to meet the capital norms.

Thus, value migration is accelerating in BFSI.

IT –

In last decade, Indian IT industry was in high growth trajectory. It was driven by cost – led value migration. But industry reached the stability phase once the market share gains and profit margins started to settle. But now the changing priorities are clearly visible. Next level of savings is offered by automation which will make location irrelevant. Client’s technology systems are changing. Digital transformation is needed to survive threat from born in cloud organizations. Indian IT industry needs to replace traditional stream revenue with new ones.

Oil and Gas –

In recent years, rising pollution is a key concern while making policies. According to WHO, half of the 20 most polluted cities globally are Indian. Various policies like Hydrocarbon Exploration Licensing Policy (HELP), Open Acreage Licensing Policy (OALP) etc. are expected to boost domestic gas production.

There’s a lack of infrastructure. But government’s focus on battling pollution by taking initiatives in gas sector can help in increasing demand. Small scale LNG is yet to take off in India. Companies have announced their intentions. But with enabling policies, improvement in pipeline infrastructure etc. whole gas sector is likely to benefit. Importers would be the biggest beneficiaries, as demand will increase and domestic gas production is unlikely to keep pace.

Consumer – Jewelry

The core drivers for jewelry such as rising disposable incomes, changing consumer preferences etc. remain relevant. Other drivers have emerged that are – GST implementation has tilted the balance in favor of organized layers. Unorganized players will have further disadvantage because of more stringent rules being introduced. Unorganized players also have lower credit availability after breakout of Nirav Modi scam. Companies are also taking initiatives in the form of exploring the unexplored segments of businesses. According to World Gold Council (WGC), gold demand was flattish or declining for past 3 quarters. Overall there was no increase in market size but Titan Company’s market share increased.

Understanding Covid-19 Impact on Cement Industry

What I Understood?

Due to Covid, government imposed lockdown in March and companies were unable to operate for a few days. In this lockdown, many labours migrated to their hometowns and thus when factories were started again there was unavailability of labour. Construction in metro cities took a halt due to lockdown and thus demand of cement was not there. Even after lockdown was lifted construction is not started with the same pace so demand is yet to increase in these cities.

On the other hand as the labour migrated to their hometowns they didn’t had much work to do. So they took the work of either constructing or repairing their own houses. Also people who wanted to start construction didn’t start but the ones who had started their construction began to finish the work. Also demand can increase before monsoon because people will try to finish some work before monsoon.

So on current situation rural areas led the demand. Now as the labours will migrate back to cities around Diwali cement demand can be increase at a substantial rate.

On costing front, some companies saw increase in freight cost while some managed it by selling higher volumes. Overall, according to companies, there were no major changes in cost.

On CAPEX, companies are delaying their CAPEX plans. One major CAPEX is done on WHRS installment. Companies are going to install WHRS which will help in reduction of fuel cost. Other CAPEX programme such as expansion of grinding units, maintenance work etc. will be delayed and also some amount of CAPEX will be reduced depending on company to company.

Sources used – https://drive.google.com/drive/u/2/folders/1BGzJuQW8pvCkiiImNXMCRYy3yrSrfRsb

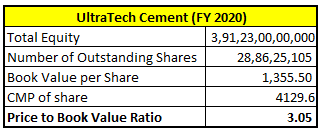

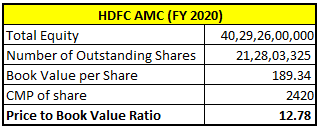

Price to Book ratio – A Wrong Metric for Service Business

What is Price to Book Ratio?

This ratio calculates the market value of share to its book value. Book value is the net assets of the company. Market price is the current price of the share.

Formula – Market Price per Share / Book Value per Share

This ratio is used by investors to check whether they are overpaying for a particular company’s stock or not.

This ratio can be a bane for service industry because in service sector companies the main assets are its employees and the cost of those employees is deducted in profit and loss account. Hence, the main assets are not on balance sheet and thus lower assets.

Let’s take two examples to interpret this.

We will take two companies i.e. one is asset heavy and other is engaged in services. For one company its assets are on balance sheet and for another its main assets are on profit and loss account.

As we can see, price to book ratio of HDFC AMC is coming higher but it cannot be said that the investors are overpaying by seeing only this ratio. As the company is mainly engaged in providing services, its major assets i.e. its employees, their cost is deducted in profit and loss account and thus having lower assets and overall net assets are also lower. But in UltraTech cement which is an asset heavy company, its major assets are on balance sheet only and thus higher net assets also.

So, P/B ratio cannot be a great ratio to analyze service sector companies.

Operating Leverage Research Paper by Michael Mauboussin

“Operating leverage measures the change in operating profit as a function of the change in sales.” To check about operating leverage in a company one can check the ratio of it’s fixed to variable cost. Fixed costs are not affected by company’s sales. So if company’s sales are low, then fixed costs will dampen profit. But if sales are higher than profit will be higher too. Generally companies with higher fixed assets to total assets ratio will have higher fixed cost too. So there’s a positive correlation between fixed assets to total assets ratio and operating leverage.

Sales Growth

Sales growth forecast is done by using economic growth, industry growth. Industry growth follows an S-curve and analysts make mistake in the middle of the S-curve. To assess industry size, number of potential customers can be multiplied by revenue per customer. Mergers and acquisitions also need to be carefully analyzed as it can change the nature of company’s operating leverage. Also evidence shows that it is challenging to create value by doing mergers and acquisitions. Increasing market share can also result in increasing profitability as there is a positive correlation between market share and profitability.

Sales growth is an important value driver because it is the source of cash and affects value factors. If company is earning more than cost of capital then only sales growth creates value otherwise it destroys value.

Level of operating profit margin at which a company is earning its cost of capital is threshold margin. Company with higher capital intensity requires a higher operating profit margin to break even in terms of economic value. So threshold margin can be used to make connection between sales growth, profit and value creation.

Value Factors

Operating profit margin can vary based on sales. To sort out cause and effect of changes, value factors can be considered.

Volume – Volume changes lead to sales changes and thus can influence operating profit margin by operating leverage and economies of scale.

Price and Mix – Change in price can impact margins i.e. if a company sells same units at higher prices then margin will rise and vice versa. Warren Buffet argued that “the single most important decision in evaluating a business is pricing power.” To assess pricing power, price elasticity can be used.

Operating Leverage – Preproduction costs i.e. investments done before generating sales and profits are capitalized on balance sheet and are depreciated later on. These costs lower operating profit margin in short run. But as the sales rise, operating margin increases because the incremental investment is small. Capacity utilization can be used to assess operating leverage.

Economies of Scale – Economies of scale is that a company is able to lower its cost per unit by producing higher quantities. Economies of scale lead to greater efficiency as volume increases.

Cost Efficiencies – These efficiencies can come in two ways i.e. company either reducing cost within an activity or it can reconfigure its activities.

Financial Leverage

Debt increases the volatility of earnings because interest has to be paid. Adding debt creates more volatility in earnings. Higher debt to total capital ratio is consistent with higher financial leverage but holding substantial amount of cash distorts this relationship.

Credit ratings are a proxy for financial leverage. Companies with higher ratings generally have low debt, higher margins, and good interest expense coverage ratio.

Threshold and Incremental Threshold Operating Profit Margin

Threshold margin is the level of operating profit margin at which the company earns its cost of capital. If the company is earning more than its cost of capital then it is creating value. Incremental threshold margin captures the margin required on new sales.

Summary of “How to Lie with Statistics” by Darrell Huff

This book tells us about how we can be tricked using different tools of statistics. We can see statistics in our daily life like in toothpaste advertisement, in company’s annual reports, in different kind of surveys etc. But if we don’t know the exact essence of this data, we can be easily fooled by this data. This book gives an idea on how to interpret this data in a more correct sense.

Sample with the Built-in-Bias

When a data is studied in statistics it is based on a sample. Now, this sample can be anything. Without knowing the details of actual sample, if we interpret this data we can go wrong. The best example for this can be the average income. In many different surveys we can see this line “The average income of this group of people is Rs. X”. If we blindly follow this data then we can be wrong because we don’t have knowledge about the sample like who participated, were they of same group, and the biggest gamble we play here is we believe they aren’t lying. If they are lying then the data is of no use. In the same way if the sample does not comprise appropriate group of people then it can mislead anyone reading this data. Author has given different example to explain this. We can take another example of marks of students. If one wants to prove that a particular class has higher average marks than others then he will include only those students in the sample who have good scores.

Different kind of Averages

When anyone talks about average most people think that it is about simple average. But wait, there are two more averages i.e. Median and Mode. The same data with no change can be shown in three different forms. Mean will depict a story, median will depict another and in the same way mode will have a different story. Statisticians or say anyone presenting a data will use an average which will best show his data. Although meaning of these three averages is different but overall they all are averages.

Here we can take an example of marks of students. The mean, median and mode can be different here depending on the marks of the students. So on asking what the average marks of the students is, it is necessary that one knows about the average used.

Missing the little ones

While studying data in statistics there are a lot of factors to see upon. These figures could be small also which many people ignores. And here they are tricked. Suppose a company wants to show that the product which it is manufacturing is effective, it will conduct surveys and will ask people to use those products and later give their results. As the company wants the result to be effective, it may happen that survey is conducted on a very small number of people and the results turn out to be in favour of company. Even if things go wrong they can conduct the surveys again because small surveys doesn’t cost too much. We can take another example of tossing a coin. If we toss a coin ten times, it may be that eight times head appears and the probability of head coming up is 80%. But if the coin is tossed 100 times then the result may wary. One should also not a follow number blindly. Say if you went for camping and you selected the place for camping by seeing its average temperature. In this case it is necessary that the range must be focused upon. It can be that the temperature ranges from very low to very high. So missing these small but important points can mislead anyone easily as these points are not given that importance.

Ignoring the Errors

While calculating any data point in statistics there could be some or the other thing which isn’t considered. Due to this the data point obtained can’t be trusted because there could be an error in this. Say for example, while conducting surveys it is not necessary that everyone is telling the truth. So there can always be a margin of error. This error can be due to ignorance of qualities, or people lying etc. While calculating IQ of students, qualitative figures are ignored like leadership skills, creative skills etc. So this IQ could also have error. And hence error should be considered while studying any data point.

Playing with the Graphs

Many people use charts or graphs to present the data in a much better way. Like if there is any trend it can be observed from it. But this chart can be easily manipulated. The data it is depicting will be correct but if the way of presentation is changed then the story can be changed. Let’s take an example. A person wants to show the increase in cases of a particular disease. Say for example he is showing increase over a period of 1 year. Cases started from zero and went up to 1000 at the end of the year. Now on the ‘x’ axis he will plot months and on ‘y’ axis he will plot cases. If he takes the scale on ‘y’ axis as of 100 cases on 1 centimetre the observer will see that the hike in cases was high. But if the scale is taken in thousands then it will look like there was not a bigger hike. In this play, charts can be manipulated.

One – Dimensional Picture

Apart from line charts, bar charts can also be used to manipulate the way of presentation. Let’s take an example. You are showing the number of corona virus patients over two different time periods. Let’s say the cases have doubled in this period. In first bar the cases were 1500 and in next bar the cases are 3000. As the cases have doubled the second bar would also be double in size. So the viewer will get that the cases have doubled. But if this same thing is applied in pictorials too, it will depict a whole new story. Author took example of cows to explain this. If the number of cows in a country has doubled and the pictorial shows two cows in which the second one is almost double in size then a person will think that the size of the cows is increased and not their population.

Semi – Attached Figure

In statistics, there are a numerous methods to misinterpret data. One such method is semi attached figures. The figures counted and the ones which are reported sounds the same but is not the same. Say for example, a report shows that “X” number of people were dead in rail accidents. People will believe that all this persons were travelling in the rail. But this figure also includes the people who were in their car or two-wheeler and had an accident with rail. So the number sounds the same that this many people were killed in rail accident but it is not the same. This semi attached figures can easily mislead anyone. In advertisements also this kind of numbers are shown. Like any chips packet with a label 10% extra. Extra of what! So one must be aware of this kind of trick and should not fall for it. A number can be presented in many ways and hence its actual jest may not be able to grasp by readers.

Post Hoc Rides Again

There are a lot of data where the person presenting it would have used correlation between different things. On seeing this correlation for the first time, it would look like there’s no problem in this i.e. it is appropriate. Having a correlation means one factor is responsible for the happening of other factor. But here, the correlation can be wrong also. Say for example, a study shows that people who smoke tend to have fewer score in test. Now it can be seen in both ways, as the student is scoring low, that’s why he smokes or as he is smoking very often that’s why he scores less. So there could be a wrong interpretation of the data. There may be a few cases where coincidently there’s a correlation.

Statistical Manipulation

Author is focusing on the ways through which data can be manipulated. He shares various examples to prove this. Manipulation can be done by using different kind of averages i.e. mean, median and mode. Different surveys can give you different averages for same data by using different averages. Percentage can also be used to mislead readers. Like if one person is calculating percentage for a certain data and if he wants to show the data to be higher than he can play with the base while calculating percentage. Double sided charts can also be used to mislead readers.

How to Talk Back to a Statistic

As there are many ways in which the statisticians can lie to us or mislead us. We can test it till some point. There are few questions with the help of which we can come to a conclusion on is the data believable or not.

- Who Say’s So?

Check for conscious bias and unconscious bias. Data could be suppressed for showing the specific result or units can be transferred. Charts can be manipulated due to special attention needs to be given here.

- How Does He Know?

As the surveys are conducted over a large sample, not everyone participates in it. Check whether the sample is large enough to describe the data precisely. As we saw earlier that there are many correlations also, check whether the correlation is significant or not.

- What’s Missing?

Look for the things missing in it. Like if correlation is given then whether measure of reliability is given or not. If average is given then check for which kind of average is given. Also, sometimes the factor is missing which caused a change to occur.

- Did Somebody Change the Subject?

Check if the subject is changing or not. Like for example, the definition of the subject changes. Earlier it meant something and now it has changed. Author has given example of farms. The number of farms was increased. This was due to the change in the definition of the farms in which there were lesser farms qualifying for that definition.

- Does it Make Sense?

Many numbers are just assumptions or it is derived from a formula which is not precise. In this case it is just a number and not any average.

Thus, Darrell Huff has tried to give an idea on how we (readers) can be fooled using different kind of statistical tools and how we can tackle them and interpret in a more smarter way.

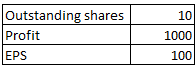

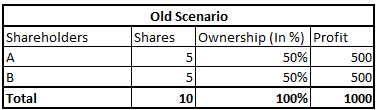

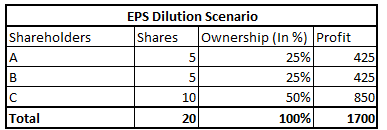

Equity Dilution v/s EPS Dilution

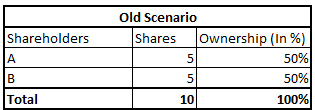

Equity dilution means change in the percentage ownership of shareholders. As the percentage ownership will change it will result in change in the profit/loss of shareholders. Let’s see this with a hypothetical example.

Assume that there is a company with 10 shares outstanding. There are only 2 shareholders both holding equal shares i.e. 5 shares each. We also assume that company earns Rs. 1000 profit.

As we have assumed that company earns Rs. 1000 profit. So let’s see how the profit will be distributed among shareholders.

In this case, both shareholders are earning profit of Rs.500.

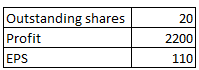

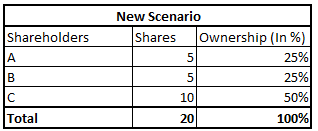

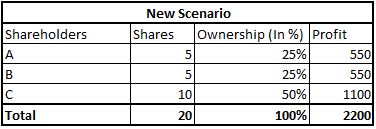

Now assume that company needs more capital and new 10 shares are issued by the company. Also we assume that new capital was used efficiently and Rs. 1200 was the profit generated on new capital.

Now, let us see how the profit will be distributed.

So in this case, earlier there were only 2 shareholders, both having percentage ownership of 50%. Profit was equally divided among them. But as they raised new capital,their profits also went up and their earnings increased (from Rs. 500 to Rs. 550). Hence their percentage ownership decreased but their earnings increased. This is called EPS accretion i.e. equity dilutes but EPS increases.

Hence, equity dilution may not lead to EPS dilution every time.

Wait. What is EPS Dilution? Lets take the same example again to understand it.

The case is same as above i.e. there are two shareholders having ownership of 50% each in a company. Earlier the profit was Rs. 1000 which was equally distributed among them. But they raised additional capital by issuing new shares and hence their equity was diluted.

But this time the capital was not used efficiently and company ended up earning a profit of Rs.700 on additional raised capital.

So let us see how the profit will be distributed now.

In this case, as the capital was not used efficiently, profits were lower which lead to lower earnings for both ‘A’ and ‘B’. This is called EPS dilution i.e. earnings decrease.

Hence, two ratios are important in equity dilution and EPS dilution concept. First is RoIIC i.e Return on Incremental Invested Capital. This shows the return company generate on new invested capital. And second one is high P/E. If company’s P/E is high then equity dilution can be profitable because company is getting higher amount.

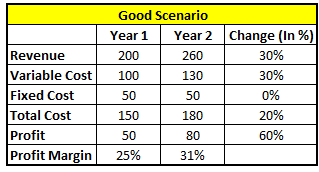

Operating Leverage

Operating leverage means company’s profit is increasing more than the increase in revenue (in percentage terms). Example – Revenue increased by 20% and profit increased by 40%.

Here we will take a hypothetical example of company ‘A’ to understand its good and bad side.

In this case company’s revenue and variable cost both are increasing. But as the fixed cost has not changed, overall percentage increase in total cost is lower than percentage increase in variable cost. Hence, profit margin is increasing.

In this case operating leverage is 2 i.e. For 1% increase in revenue, profit will increase by 2% and vice versa.

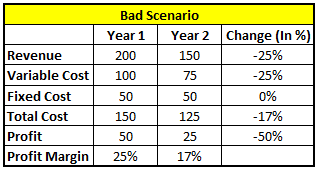

But this could turn out to be a bad scenario if market is not in a good position. Let’s see how.

In bad scenario, company’s revenue decreased by 25% and variable cost too decreased by 25%. Although, overall decrease in total cost was lower than decrease in variable cost (in percentage terms). Also, revenue decreased more (in terms of percentage) than cost. Hence profit margin was impacted.

Hence, operating leverage can be good when market is in a good position but if market takes a u-turn then this operating leverage can work in opposite manner i.e. if in good times profit was rising 2% for every 1% revenue increase (assuming operating leverage as 2) then in bad times the profit will decrease 2% for every 1% decrease in revenue.

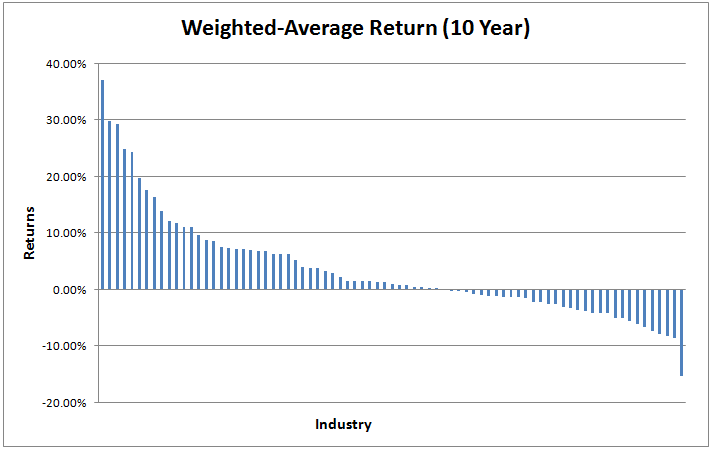

Industries Beating Cost of Capital

Analyzing industry should be the first step for investing. There are many quotes by different iconic investors on the same.

If an investor finds a good industry, he has mitigated some of his risk. How? Because if we analyze any industry for a longer horizon, say 10 or 15 years, we can have a decent idea of how the industry is (in terms of profitability). Also by taking a longer horizon, we can be satisfied by the result because any economy can see different phase of economic cycle in 10 or 15 years.

Nature of industry doesn’t change overnight. Example – A tyre industry’s nature will not change in short term (until there is something better than tyre). Tyre is the essential part of vehicles so we can say that tyre industry’s business can’t go out of fashion (although companies working in industry can).

Also Charlie Munger, also known as wisest man alive on Earth, quoted “Fish where the fish are”. This means that if there are two ponds (take this as industry) which have 10 fishes each (fish could be taken as companies). But one pond has 7 rotten fishes and second one has 3 rotten fishes. Where would you fish? Obviously second one because the probability of getting a rotten fish is less in second one.

In the same way, if an industry has companies that are earning profits above their cost of capital for a longer time then it can be taken as a good industry and vice versa.

So, today we have analyzed almost 80 sectors of Indian economy. We have taken RoCE i.e. Return on Capital Employed for the calculation of economic profit. Although RoIC i.e. Return on Invested Capital would have been a better measure but we have taken RoCE as a substitute to RoIC. Also we have taken weighted average because there were some companies having extremely higher return but there overall weight in industry was low. This was portraying wrong image of industry. But with the help of weighted average, the return was normalized.

Here is the excel file where all the calculation is done.

Done by Sanjeel Kothari and Kusum Chaudhary

Summary of Book “The Five Rules for Successful Investing”

For Summary of Chapter 1 to Chapter 6 click on this link: https://thefundamentalmindset.finance.blog/2020/05/10/book-summary-of-the-five-rules-for-successful-stock-investing/

Chapter 7: Analyzing a Company – Management

Analyzing management of business can be a good step for investors. Management team should be like who thinks as shareholders. Management can be a difference between a good and a bad business. There are three ways in which management can be assessed – compensation, character and operations.

Compensation –

Compensation is easy to assess because majority data is available on a single document. One should check that in which way the management is paying itself i.e. bonuses, share grants, big salaries etc. Compensation of competing firms can also be checked to see what competitors are paying. It also depends on company to company i.e. big companies can give higher salaries, bonuses etc. Many companies pay according to the performance delivered by manager. If a firm is changing targets without changing compensation then this can be a red flag. Basically compensation of managers should be decided according to the performance of the company. There are some points which could be a red flag like if the company is paying for expenses which were to be paid by manager or is company giving loans to managers and then forgiving it or executives having too much skin in the game etc.

Character –

To determine whether a firm’s management deserve investor’s trust, few questions can be useful like checking related party transaction, checking board members (whether it comprise more of family members or not), whether company is able to retain talent, whether management is taking decisions that can hurt financial statements but gives more clear picture of company.

Operations –

Compensation and trusting the management is ok but the main sign is that whether the business is running properly is not. It can be checked through – analyzing numbers such as ROE’s, ROA’s etc. focus should also be on mergers and acquisitions, by analyzing steps decided by management (whether they are followed or just renewed every year), is proper information is provided or not for analysis, decisions which make firm flexible etc.

These things if analyzed properly can give a good picture about company’s management.

Chapter-8: Avoiding Financial Fakery

Company’s can use accounting to their advantage by employing dozens of techniques that, though are legal, may provide an observer a false picture of a company’s performance. This is known as Aggressive Accounting.

An outright fraud is worst than aggressive accounting detecting the signs of a potential fraud can save from a loss. Although Professional assistance may be required to understand how is a company exaggerating it’s result, it’s not difficult to recognize the warning signals for the same.

Six Red Flags

There are six major red flags to watch out for before giving a firm a clean check:

Declining Cash Flow: The most simple thing one can do to analyze a company’s health is to watch the cash flow. A company’s cash flow from operation should follow the same path as its net income. If cash flow from operation declines or doesn’t grow at the same rate as net income grows, it usually means that the company is generating sales without collecting cash which may prove fatal for a company.

- Serial Chargers: One time charges and write downs usually affect different accounts which need to be adjusted to facilitate year to year comparison of financial results. Frequent charges are an open invitation to accounting frauds because companies can bury its bad decision in the name of such one-time charges.Big restructuring charges are incurred to improve company’s future performance by bearing future expenses into the present. All those decisions which are poor may get rolled into a single one-time charge which improves future results.

- Serial Acquisitions: Firms that make numerous acquisitions need to restate their financial more frequently. There’s a huge amount with such firms because acquisite firms spend much lesser time to check out their targets than they should.

- The Chief Financial Officer or Auditors Leave the Company: The people who watch the company’s financial performance are its chief financial officer or the auditors if any of the two leave the company for vague reasons specially for a company which is already under a suspicion for an accounting issues should be an eye opening signal.

- The Bill’s Aren’t Being Paid: One of the ways for a company to increase its growth rate is to loose in customers credit term, which motivates them to buy more goods and services. However loose credit term may invite shakier customers the result of which will be a charge against earnings for the company in the future.

To track this risk the rate of increase of account receivables to the rate of increase of sales can be tracked.

Also the allowance for doubtful account can be tracked to see how much money the company won’t be able to collect from debt beat customers. If this amount doesn’t go up with account receivable, the company may be artificially showing it sales at a much higher amount by not recognizing those customers who aren’t expected to pay their bills.

- Changes in Credit terms and account receivables: Checking the company’s 10-Q filling will help to know any changes in credit terms from customers and any explanation by management as to why AR has increased.

Seven Other Pitfalls to Watch Out For

- Gains from Investments: It is common for big firms to invest in other companies. An honest company reports sale of these investments separate from it sales and reports it below the operating income line on the income statement. However, some companies may use this income to boost their result by including it as a part of revenue or by recording it above the line thereby including it as a part of operating income.

- Pension Pitfalls: The Company invests in stocks, bonds, real estate and other asset classes to fund future pension payments. However if the company has fewer pension asset than pension liability it has an underfunded plan which means it has to divert the profit to meet the gap. In the footnotes of a 10-k filling two keys numbers namely projected benefit obligation and fair value of planned asset at the end of the year can be compared to identify whether a company has an over or underfunded pension plan. In case of an underfunded pension plan the company need to divert hard cash to fund the plan instead of distributing it to the shareholders and increase the firm’s value.

- Pension Padding: When pension assets do well and the return on those assets is greater than the annual pension cost the excess can be counted as profit.However this strange kind of profits can’t be paid out to the shareholders as it belongs to the pension holders. The excess thus benefit the shareholders because the company needs to contribute less in the pension plan in the future. However this income is dependent on the stock market and thus must be subtracted from net income to figure out how profitable a company is really is.

- Vanishing Cash Flow: Employees of a company exercise the stock options the amount of cash taxes that their employer has to pay decline. This means that as long as the firm stock price is going up and it is giving out options the cycle continues. More options are exercised and more deductions are taken. However if the stock price decline fewer option will be exercised resulting in higher taxes for the company. Thus checking that the company’s cash flow growth isn’t coming from option related tax benefit it comes crucial.Thus if inventories are rising faster than sells, the company may be in trouble. (Unless the company is preparing for a new product launch)

- Overstuffed Warehouses: When a company is producing more than its selling, either the demand has decreased or the company has been overly ambitious in forecasting demand. In both the cases the unsold goods will have to be sold at discount or written off. This would result in a big charge to earnings.

- Change is bad: Firms may choose to alter certain assumptions in their financial statements to make themselves look better. Increasing the estimated life of an asset so that annual depreciation reduces can be a way to inflate earnings. Not providing for the irrecoverable amount of debtors in the doubtful account may pose a picture that the firm is stretching the truth which will come back as charge to the earnings at some point in the future. Other things related to how expenses and revenue is recognized can be changed to alter the presentation of financial performance.

- To expense or not to expense: There are certain expenses such as marketing costs and software development which can be treated either as a capital expenditure or as revenue expenditure. However it may so happen that the company treats certain expenses as capital expenditure so that instead of charging the entire expenditure to the current year earnings, it is spread out in a few years to come.

Chapter 9: Valuation – The Basics

Analyzing company’s management and checking its financials can help filter good companies but if they are purchased at too high a price then it is not a worth investment. In bull market of 1990’s and tech bubble people were ready to pay high amount for a stock. Valuation was completely ignored.

Stock market’s return depends on two key components – investment return and speculative return. Investment return is the appreciation in stock price and also includes dividend growth and earnings growth. Speculative return is impact due to changes in P/E ratio.

If P/E doesn’t change and earnings and growth increase over time then investor can earn good returns as compared to a scenario where P/E has decreased.

Starting with valuation, first step can be to analyze traditional ratios such as P/E or Price-to-Sales. Price to Sales (P/S) can be a good option because it measures price of share by sales per share. Sales can be a good option because companies mostly use tricks in earnings (in sales also tricks could be there but it is identifiable). One catch in P/S is what if company is aggressively posting sales but is earning less on these sales. P/S ratio should be used to compare companies with same profitability.

Price-to-Book is another way for valuation. It measures stock’s market value with book value. It is more effective in companies with good tangible assets. Companies using intangible assets have little use of P/B ratio because most intangibles are not directly added to book value. Goodwill can cause an expensive firm to look like a value firm because it inflates book value. ROE also impacts P/B ratio because higher the ROE means company is compounding book equity at a higher rate. P/B can be a good method to value financial firms because many of their assets are revalued every quarter.

Coming to P/E – one of the most popular valuation ratios. P/E can be compared for two firms or for a firm for different periods. P/E can be affected by different things like capital structure, risk levels etc. But comparing a firm’s historic P/E with current P/E can be useful. Drawback of P/E is that relative P/E is neither good nor bad. As P/E depends on future cash flows, capital needs, a single number can’t tell proper valuation. Company which is expected to grow at faster rate will have high future cash flows so it can have high P/E. Also a firm with high debt can have low P/E. There are some questions which can be helpful while analyzing P/E ratio like if any business/asset was sold recently or is the firm cyclical or if the firm has taken any big charge etc.

PEG Ratio is also popular among some investors because it takes in consideration growth rate also. It makes sense because if the company has high growth rate its value will be more in future. Risk should also be taken care of. While analyzing PEG ratio one assumes that risk will be equal which might not be the case.

Apart from multiple based measures, yield based measures can also be considered. Example – we can invert the P/E ratio i.e. divide earnings by market price. By this we get earnings yield which can be helpful in comparing yields of different products. Analyzing cash return is also a good measure. It shows how much free cash flow the company has generated.

Chapter-10 Valuation:- Intrinsic Value

The drawback of using ratio to value stock is that ratio only allows relative comparisons. It means it only helps to compare one company to another.

However knowing the intrinsic value of the stock helps you to know how much you should pay for the stock. Having an intrinsic value helps you to focus on the core business. It forces you to think about present and future cash flows as well as its return on capital. Also it gives you a stronger basis for making investment decision.

Cash Flow, Present Value, and Discount Rate

The value of a stock is equal to present value of future cash flows. Companies create value by investing capital and generating a return. A part of that return is operating expenses, another part is reinvested in the business and the remaining is the free cash flow. These free cash flows are taken to account by estimating the value of a stock.

Cash flows in the future are worth less than those received in the present because there is uncertainty about the future and present cash flow can be invested to get a return on them. The chance that we may not receive the future cash flows needs to be compensated through risk premium. The addition of the government bond rate and the risk premium is just the discount rate. It is the rate of return you would need to make for the indifferent between money receive in present and in the future. Because of this concept the stock with stable and predictable earnings often have high valuation due to lower discount rate.

Calculating Present Value

The present value of a future cash flow in year capital end equals CFn/(1+R)^n.

Fun with Discount Rate

There is no precise way to calculate the exact discount rate. As interest rate increase, so will the discount rate.

The factors which need to be taken into account by estimating discount rate are:

- Size: Smaller firms are riskier than larger firms because they are more vulnerable and are less diversified.

- Financial Leverage: Firms with more debt are generally riskier than others because they have a higher proportion of fixed expenses which will benefit them in good times but make it worse for them in bad times.

- Cyclicality: The cash flows of cyclical firms are tougher to forecast than stable firms.

- Management/Corporate Governance: It refers to the level of trust and the way a management operates. Companies with management which show red flag are definitely riskier.

- Economic Moat: The stronger companies competitive advantage the more likely it will be able to avoid competition and generate a consistent stream of cash flows.

- Complexity: The more complex the business, the more are the changes of something unpleasant happening. A complexity discount can be incorporated to provide for this risk.

Calculating Perpetuity Value

After having the cash flow estimates and the discount rate we need a perpetuity value to put the whole thing together. We need this value because it’s not possible to estimate a company’s future cash flow out to infinity.

To calculate this value take the value of the last cash flow that you estimate (CF), increase it by the rate at which you expect cash flows to grow over the very long term (g) and divide the result by the discount rate(R) minus the expected long term growth rate(g).

Formula: CFn(1+g)/(R-g)

Discount this result to arrive at the present value.

Add the discounted perpetuity value to the discounted value of our estimated cash flows and divide by the number of shares outstanding.

Margin of Safety

After valuing a stock, we need to know when to buy it. As an investor, you should seek to buy companies at a discounted estimated value. This discount is called the margin of safety.

Having a margin of safety is like an insurance policy that helps us prevent from overpaying and mitigates the damage caused by overoptimistic estimates.

This margin is different for different stocks. It all depends upon the characteristics of the business like pricing power, market share, stability of demand, etc. The price you pay for a stock should be closely tied to the quality of the company. Having a margin of safety is critical to being a difficult investor because it acknowledges that as humans, we are flawed.

Conclusion

Every approach to equity investing has its own limitation. Sticking to valuation may mean that you will miss out on some great opportunities.

Chapter 11: Putting It All Together

In this chapter, whatever things are taught in the book from starting, are applied on two companies.

Case of AMD (Advanced Micro Devices) –

On reading news or going through company’s website it might look a attractive investment opportunity because it is one of the only two firms in the manufacturing of microprocessors. Also the company is working on a powerful next generation chip which could be better than what Intel could offer.

On analyzing economic moat, it was seen that AMD was making money in times of boom and losing money in normal times. Overall, there was no such sustainable economic moat.

Growth was volatile and profitability was volatile too. It was not efficient in spending. On checking financial health of company, it was found that debt to equity ratio was not high and current ratio was also not poor. But the company lost a substantial amount of money too. On preparing a bear case, management’s compensation was checked and a red flag was raised because even in the year when company was losing money, management team was getting high salaries and bonuses.

Valuation was tough for AMD as it has lost money in past two years and also the share price was higher than what the valuation gave.

Case of Biomet –

Biomet’s business was more promising. Margins are fat in this industry. Also firm is in market from 25 years so it has a trusted customer base.

On analyzing economic moat, it was found that free cash flow, operating margins and net margins were good. On analyzing financial results, it was found that in 1999 company had to pay a charge on legal dispute which was a onetime charge. All else was good. On analyzing factors such as growth and profitability, it was found that growth was a little volatile but sales growth was average. Gross margins are high and have increased over time. SG&A costs have been steady and research and development expenses are declining but this could be taken as a positive sign because company is spreading it over higher sales base. On financial health front, company has no long term debt and current ratio is also high.

On preparing a bear case, it can be concluded that legal disputes can be there in future and also Biomet’s foreign operations are not much profitable. Biomet’s market size is also low compared to industry leaders.

On analyzing management compensation, it was found that management team is taking reasonable amount and options are used responsibly among employees. On doing valuation it was found that share was trading at higher price and by changing scenario it was found that the current market price is near to the valuation outcome.

Chapter 12: The 10-Minute Test

Does the firm pass a Minimum Quality Hurdle?

The first step is to avoid the junk among all the companies. Those companies with very small market capitalization and those that trade on bulletin boards must be avoided. Also those foreign firms that don’t file regular financials must be avoided.

IPOs must be avoided as they there young with short track recorders. However spun off companies aren’t exceptions to this and may prove to be attractive.

Has the company ever made an Operating Profit?

Those companies which are in the money losing stage sound exciting but usually have only a single product or service to offer. Such stocks may blow up your portfolio and thus must be avoided.

Does the company generate Consistent Cash flow from operations?

Those companies which don’t generate enough cash flow or report negative cash flow from operations have to seek additional financing by selling bonds or issuing shares. Both the sources have their own limitations.

Are returns on Equity consistently above 10 percent, with reasonable leverage?

The minimum ROE for a non-financial firm can be taken as 10% and for financial firms, 12%. However the ROE generated must not be a result of the use of leverage.

Is earnings growth Consistent or Erratic?

If the company doesn’t have consistent growth rate it is either in an extremely volatile industry or competitors have an edge over it. The former is not bad if the long term outlook is good, but the latter may prove to be a big problem.

How clean is the balance sheet?

Firms having a lot of debt require extra care because of their complicated capital structure. If a non-bank firm has a high financial leverage ratio or a high debt to equity ratio ask yourself the following questions:

- Is the firm in a stable business

- Has debt being gown down or up as a percentage of total assets

- Do you understand the debt

Does the firm generate free cash flow?

Those firms which create free cash are preferred over others because it is the cash generated after capital expenditure which increases the value of the firm.

However if the cash generated is being invested in good projects than, negative cash flow can also be considered.

How much ‘Other’ is there?

If a company repeatedly shows huge one time charges in its financial statements, it may show that the company is hiding its bad decision.

Has the number of shares outstanding increased markedly over the past years?

If this is the case, the company is either issuing new shares to buy other company or granting numerous options to employees. Most of the acquisition fails and granting option means diluting the stake of the shareholders.

However if the number of shares are decreasing it means firms are returning the excess cash to shareholders. However stock repurchases are good only when the company’s share are trading for a reasonable value.

Beyond the 10-minutes

After a firm passes this test, a summary of its financial statements, its 10-k filing, the management and discussion analysis, its compensation policy and all the other major documents can be gone through to get an idea on its business and everything going on in the company and its sector.

Chapter-14 Health Care

Healthcare is one of the few areas of economy which is directly linked to human survival. Giving the importance for healthcare and a free regulatory environment enables the sector to score above average financial return, Healthcare companies are often highly profitable with a strong free cash and return on capital.

The sector experiences consistent demand as well such as drug companies, biotech, medical device firms and health care service organizations.

Economic Moats in Health Care

Economic moats in the sector include high pack up cost, patent protection, significant product differentiation and economies of scale. These factors create entry barriers as the established big players already excellent in these areas thereby leading to great profitability.

Developing drugs can take several years of research and development and can cost millions over that time frame. This creates a huge entry barrier, which even if surpassed would require a lot of promotion to stand head to head with established players.

The sectors vast side and rapid expansion makes it an attractive investment. However it involves complex relationships, controversy and political pressures.

Role Of the United States Food and Drug Administration

After passing through all the above stages, the toughest stage is yet to come. Once a drug passes the phase 3 testing, a new drug application needs to be filed with the US FDA. It takes about 17 months for FDA to review an application and that too with a 70% chance of approval.

The FDA has advisory committees that meet several times in a year to discuss the application and submit their opinion to the FDA thereby, deciding the fate of the drug.

If the FDA isn’t convinced, a not approvable letter is sent to the company.

Patents, Intellectual Property Rights, and Market Exclusivity

Once a drug is approved by the FDA, the marketing can begin. Drugs generally enjoy patent protection for 20 years from the date the company first completes the patent. However, because a patent application is usually filed as soon as the drug is identified a significant portion of the period is eaten up by trials and approval process. Thus many drugs enjoy only 8-10 years of patent protection after they have been launched in the market.

The information about a drug company’s patent protection can be seen in the 10-k report under the heading “Patents and Intellectual Property Rights”.

Generic Drug Competition

After a drug goes off patent, it is open to competition from generic medications. Generic drug has the same chemical composition with a 40-60% lower price. A firm can lose a significant portion of its sales if it is over dependent on one single drug for its sales.

Hallmarks of Success for Pharmaceutical Companies

Companies that provide stellar performance focus on these traits:

- Blockbuster Drugs: These are drugs with more than $1 billion in sales. Companies with such drug gain manufacturing efficiencies by spreading fixed cost over more products.

- Patent Protection: Every drug eventually loses patent protection, but those companies who manage the losses best will generally provide investors with a more consistent stream of cash flows.

- A full pipeline of drug in clinical trial: It refers to having an abundance of products in development and directing research efforts towards unmet medical needs.

- Strong sales and marketing capability: Pharmaceutical salespeople are the ones who act as a link between the company and the physicians. The relationship of companies with professional medical staff is very valuable for a drug firm.

- The big market potential: Those drugs that treat conditions affecting a large percentage of the population have a better potential than niche products.

Generic Drug Companies

Generic drug makers do not have extraordinary margin but are growing much faster due to their increasing popularity. The return on invested capital varies dramatically depending upon the company’s exposure to branded drug.

Generic drug companies can benefit from competitive barriers. The first company to filed a legitimate patent challenge against a branded drug enjoyed 180 days of market exclusivity.

Biotechnology

Biotechnology firms need to discover new drug therapies using biologic cellular and molecular processes rather than the chemical processes used by big pharmaceutical. These firms are also concern with developing therapeutic products.

The greater product risk under this sector because the therapies are often completely new forms of treatment.

Hallmarks of success for Biotech Companies

Three categories into the biotech firms can be divided:

- Established: These include the biggest companies of biotech sector which have annual product revenues of more than $1 billion. These companies have positive earnings and cash flow. Characteristics:

- Large numbers of drug in late stage clinical trials.

- Plenty of cash on hand and cash flow for research and development expenditures.

- Stock having a margin of safety of around 30-40% of its fair value

- Sales sustaining salesforce

- Up and Coming: These firms are on the verge of breaking into the black or those which have already demonstrated small but positive earnings. These firms are a lot riskier and have no economic moat. During this stage companies require a lot of cash for the last phases of clinical trials and for preparing documents for the FDA.

- Speculative: These are companies which make up the majority of all the companies in this industry and are too risky. These firms may have interesting technologies and may become extremely successful one day, real revenues are many years away. The odds of drugs of each company reaching the market are very low and thus a huge margin of safety is required while investing in them.

Medical Device Companies

These are the companies that make hardware for medical procedures. There are two types of device firm – Cardiovascular and Orthopedic. An increase in the aging population and in the life expectancy will drive growth in medical devices. Due to a pressure on medical cost if the demand for medical device company has increased as it reduces the cost of some procedures. Medical device companies have wide economic moat like economies of scale, higher switching cost and long term clinical history. Patent Protection also provides a measure of avoiding competitors.

These companies have a great deal of pricing power as well. Due to absence of substitutes the firms have been able to raise their prices by 3-5% every year.

Device firm are not without risk. Product cycle can be very short and thus expenditure on research and development has to be incurred to keep up with the competitors. There is also legal risk involved.

Hallmarks of success for Medical Device Companies

- Salesforce Penetration

- Product Diversification

- Product Innovation

Health Insurance/Managed Care

Insurance or managed care firms are subject to intense regulatory pressure making them less attractive than other health care industries. They don’t have wide economic moats. Stocks must be chosen carefully and a huge margin of safety is required for investing in this companies.

One of the ways insurer rise to gain pricing control or by creating Managed Care Organization. MCOs make money in two ways. One is by underwriting medical insurance which is known as risk based business. The other way is by simply administrating services known as Fee based business. Companies with a greater proportion of fee based business less risk because of more predictable cash flows.

Hallmarks of success for Health Insurance/Managed care companies

- Effective medical cost management and underwriting: The medical loss ratio calculated by medical cost paid divided by premium revenue. It is the best measure of the firm’s effectiveness in this area. This ratio reflects a company’s overall success and consistency in managing its risk based business.

- Minimal Dual Option Business: Managed Care organization provides individuals the opportunities to choose from two or more types of plan. Companies with a large portion of this dual option must be watched out for due to the risk of mispricing.

- Large mix of Fee based business: Having a large proportion of fee based business as compared to risk based business is always a positive in our book. Minimal exposure to Government accounts: Companies with less exposure to government accounts will outperform those that rely on government revenues.

Chapter 15: Consumer Services

Consumer services firms have a very narrow economic moat generally. Even if a firm has any unique product it does not remain unique for a long time. There are very few firms who have managed an economic moat by offering ready to eat/ quick to prepare food, some stores give 24/7 services or some stores have checkout at the front of the stores. Any firm giving these kinds of services at competitive price can outperform its competitors.

Major industries in consumer services –

Restaurants –

This industry can be divided into two segments i.e. quick service restaurants (fast food) and full service restaurants. As both the spouses are working they get less time to cook food and also to buy groceries. So the preference for going out and eating at restaurants has increased.

Now comes investing in these companies. Many restaurant concepts start and after a few time they either fail or they grow. But during this time their earnings may be negative or inconsistent. Those which grow, expand their business by opening new stores. Many times new store are aggressively opened and then again cash flow turn negative. When expansion is not possible it becomes important that profits are generated by existing units. Even when restaurants have reached at the stage of slow growth, it is possible for them to survive by providing what customer wants and by advertising and service. If these things are not done properly then restaurants may decline.

Retail –

Two major facelift in past decades were – development of category killers and one stop shopping experience. Some firms developed the method of providing goods to customers at a discount every day.

Now comes investing in retail. One of the ways to differentiate good retailers from bad retailers is to check cash conversion cycle. If retailers are selling quickly, is collecting payment quickly and is paying late to suppliers can help them reduce their days in cash conversion cycle. Increasing inventory and increasing days in receivables is a sign of trouble but if there is a increase in payment to suppliers it is a good sign because company is paying late and is using goods earlier. Store traffic and good employee culture needs to be maintained by retail stores.

The only way a firm can build moat in this sector is by providing goods at lower rate because prefer to buy the same good at lower rate (if a sweater is sold for $50 and in next store the sweater is being sold for $40 customer will go for second store providing sweater at cheap rate.

Chapter-16 Business Services

Companies in this sector can prove to be those running wonderful, wide- moat businesses- the ones anyone would like to buy at the correct price and keep as long-term investments.

These companies are varied and thus are divided into three categories- technology-based, people-based, hard-asset based. Not all companies fit perfectly into any one of the three categories. Despite being such a varied business, a few factors affect the majority of companies in this sector.

Outsourcing Trend

Outsourcing refers to offloading the non-core tasks to third parties. These are tasks which the firms would find impossible to handle internally. Outsourcing saves time and cost and allows businesses to avoid the hassle of handling non-core activities on their own and allows them to focus on the main business.

Economic moats in business services

In this industry, size matters. Companies may leverage size to boost their top and bottom lines. By handling more volume over a fixed cost network, unit costs can be lowered and profitability can be increased. Many firms acquire others to achieve economies of scale.

Size affects branding as well. Usually, larger and well-known firms are preferred over others.

Many industries in the sector have huge barriers to entry making it difficult for new players to enter. Despite the companies having wide economic moats, they need to differentiate themselves to fight the intense competition in the industry.

Technology Based Business

These companies include data processors; data based providers and other companies that leverage technology to deliver their services. These companies have a sizeable and defensible competitive advantage which helps them to generate better than average long term returns.

Industry Structure:

These companies offer the strongest cases for outsourcing. These firms require huge initial investments to step up an infrastructure that can be leveraged across many customers. These investment acts as an entry barrier.

In this market price competition tends to be less intense. Rather the companies prefer counting on enough growth to go around for all companies to benefit.

Low ongoing capital investments are very low in this sector because of the huge upfront technology investments that have already taken place.

Companies benefit from both economies of scale and operating leverage. The combination of operating leverage and low capital requirements suggests that these firms have plenty of free cash.

Companies in this sector have predictable sales and profits due to long term contract. This means that 80-90% of a company’s revenue can be booked even before the year begins.

Hallmarks of success for technology based business

- Throw off cash: Big market opportunities, operating leverage and minimal ongoing investment requirement enable these businesses to have free cash flow margin.

- Enjoy economies of scale: The figure players in the industry benefit from cost advantages relative to other small competitors which translates into better financial performance.

- Report stable financial performance: Due to long term contract, the majority of revenues are recurring and predictable for these firms.

- Are exposed to fast growing or under penetrated markets: Due to the operating leverage, exposure to market with lot of growth potential should translate into impressive profit expansion.

- Offer a complete range of services: Those firms who offer a wide range of services benefit because buyers look to consolidate their purchases.

Have strong sales capabilities and excess to distribution channels: To sell business services, most successful companies have strong sale forces.

People-Based Businesses

These companies include those that rely heavily on people to deliver their services such as consultant, professional advisors, advertising agencies and temporary staffing companies.

Industry Structure

These businesses make money by leveraging and investment in their employee’s time. Growth for people-based companies comes mainly from finding and hiring more skilled workers. Training is an important component to ensure a standard level of service quality. Salary expense is a big fixed cost which must be covered for profits to be made.

Relationships are an important characteristic in this sector. Products are designed according to clients and purchase decisions may be made because of the relationship.

Brands, relationship and geographic scope can provide a competitive edge in an industry of aggressive competition.

Hallmarks of success for people-based businesses

- Differentiation of offering: Differentiation can help companies generate superior financial results.

- Providing a necessary or low cost service: When customers feel compelled to purchase a service and the cost of service is relatively low, customers need not try to negotiate for a better price.

- Organic Growth: Internally generated growth is preferred over growth generated by acquisitions as it signals healthy demand for the firms service.

Hard-Asset-Based Businesses

These are companies which depend upon big investment in fixed assets to grow their businesses. Airline, waste haulers and expedited delivery companies fall under this sector.

Industry Structure

These businesses require large incremental outlays for fixed assets. The incremental fixed investments occurred before asset deployment, and thus, companies in this sector generally finance their growth with external funding. High leverage is not a bad thing unless the cost of debt financing can be covered along with a reasonable return for shareholders.

Airlines are the least attractive investment due to their enormous fixed cost, expensive labour contracts and a non-differentiable commodity service. Thus price competition is intense, profit margins are negligible and operating leverage is too high.

Majority of these businesses fall into the narrow or no moat bucket. Thus investors should look for a steep discount to fair value before buying the shares.

Hallmarks of success for Hard-Asset-Based Businesses

- Cost leadership: Due to the large fixed cost, those companies who are more efficient have a strong competitive advantage.

- Unique Assets: When limited assets are required to fulfill the delivery of a particular service, ownership of those assets is the key. For example, landfill assets.

- Prudent Financing: Having a lot of debt is not a bad thing unless it can be financed by the cash flow of the business.

Chapter 17: Banks

Bank is one of the most important sectors in every economy because they provide the service of lending money to the businesses. In an economy, whichever business needs money can approach bank for financing. Their business model is simple. They borrow money from people at low rate and lend this money on high rate and the difference in this rate is the Net Interest Income for banks. Also they provide other services and earn noninterest income on that. Central bank of countries acts as the lender of last resort. Banks can turn towards central banks in times of liquidity crunch. Banks also get paid for the risk they undertake. Generally the risks are credit risk, liquidity risk, interest rate risk.

Credit risk and managing it –

Credit risk is that the borrower will not repay the loans given to them. Credit risk is always there in the case of banks due to their business model. Banks generally avoid this risk by either diversifying their portfolio, or through collection procedures or by solid underwriting. Banks which specialize in these activities can have an edge over competitors. Investors should keep a check on non-performing loans, charge-off rates (percentage of loans the banks think will never be repaid) and their trends. Investors can also compare this rate for different banks. Lending pattern can also be observed from bank’s financial statements.

Selling Liquidity –

Apart from credit risk, banks also have liquidity risk. Banks offer liquidity management services. Companies sell their receivables to banks for a discount to get immediate liquidity. Customers too pay for liquidity services. When the interest to be paid on deposits is less than interest earned by lending, in this case the bank is earning the spread on depositor’s money and eventually depositors are paying for it. These low cost accounts helps bank earn profits so as an investor we should check whether these accounts are increasing or decreasing. Also we should check whether the banks have given too many loans in a single sector or not because it can lead to a series of defaults. Banks should have diversified loan book.

Managing interest rate risk –

Third and one of the main types of risk faced by banks is interest rate risk. There are four major components to examine i.e. Interest income, Interest expense, noninterest income and provisions for loan losses. If interest rate falls then bank’s interest expense reduces. But generally interest rate falls when economy is facing recession or tough times. In this case defaults also increase so bank’s provisions increases too. But banks have other tools to manage risks. Banks can reposition their risks by focusing on the sector which they are lending. Big banks also have facilities to pass the loan to investors.

Economic moat in banks –